- CBDCs are more than just digital rupees or dollars; they are programmable money, sovereign code, and a combination of monetary policy and geopolitical strategy.

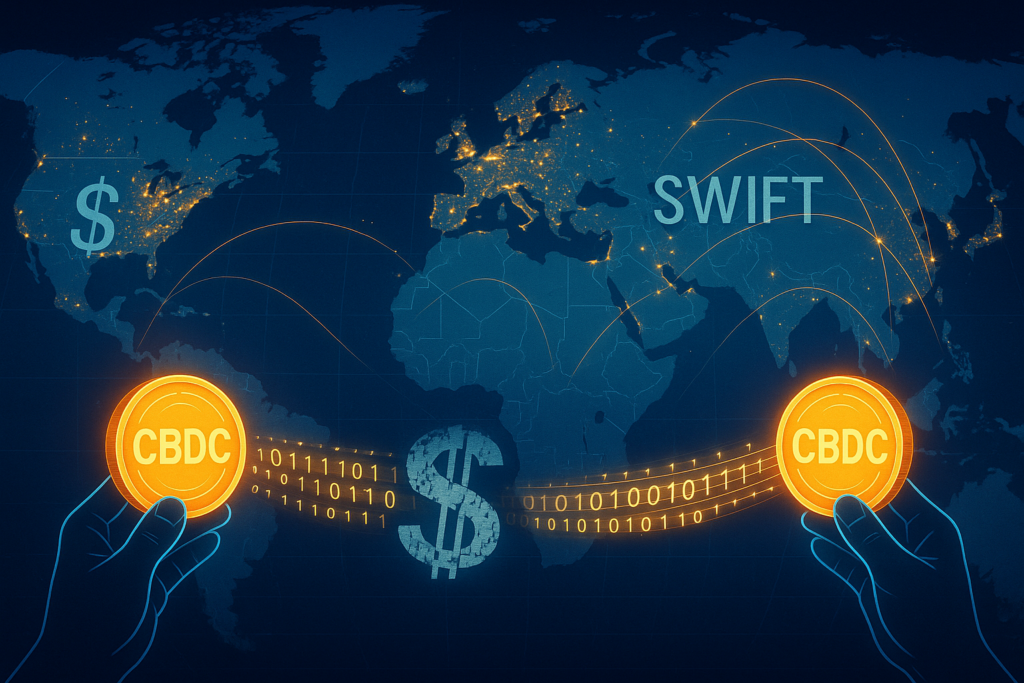

- Trade between two nations settled directly in digital currency, bypassing the dollar and SWIFT system, would weaken reliance on US-controlled infrastructure, reduce the dollar’s dominance, and open new routes for countries to sidestep sanctions and financial oversight.

- CBDCs promise a revolution by enabling fast, low-cost cross-border payments, thereby promoting de-dollarisation and multipolar trading blocs.

- The real contest ahead is not over cash, but over who controls the digital infrastructure that moves it.

After the Soviet Union’s collapse, global finance seemed to settle into a familiar rhythm—dollars, euros, and yuan flowing through trade and settlement systems, sanctions enforced through the dollar-clearing network, and power largely concentrated in Western-dominated institutions. In the aftermath of the 2008 financial crisis, when the world witnessed the collapse of Lehman Brothers and the US Federal Reserve printed trillions of dollars to bail out its banks, a quiet revolution began. The emergence of state-backed digital currencies, also known as central bank digital currencies (CBDCs), has been changing the landscape of trade settlements, sanctions regimes, and, eventually, the global financial system’s power balance.[1] CBDCs are more than just digital rupees or dollars; they are programmable money, sovereign code, and a combination of monetary policy and geopolitical strategy.[2] As over 130 countries consider CBDCs, including India with its e-Rupee[3] trial, the global financial order is at a crossroads. This isn’t just about cashless societies; it’s about currency warfare in the digital era, where control over money equals control over power.

The Dawn of CBDCs

The introduction of digital fiat currencies by central banks is more than just a payment innovation. It is a strategic action. According to economists, the issuance of a CBDC represents a reaffirmation of monetary sovereignty in the digital realm.[4] When a state issues an electronic version of its currency, it acquires tools that it did not previously have: real-time settlement, limited control over cross-border flows, potentially dashboard-level visibility into transactions, and a new geopolitical tool.

What exactly does this mean in practice?

To begin, picture a scenario in which trade between two countries is settled in digital yuan or digital euro directly from central bank to central bank, rather than in dollars or through the SWIFT-based system routed through the US. Such a change would lessen reliance on US-dominated infrastructure, erode the dollar’s leverage, and provide new paths for states seeking to evade sanctions or financial scrutiny.[5]

Concrete data demonstrates this momentum. In China, the e-CNY had 180 million wallets and cumulative transactions of over 7.3 trillion yuan (about $1 trillion) by mid-2025,[6] but adoption remains low at 0.16% of the cash-equivalent money supply, suggesting preferences for established platforms such as Alipay.[7] India’s digital rupee, piloted since 2022, saw circulation climb to ₹10.16 billion ($122 million) by March 2025, a 334% increase from the previous year, with over 6 million users and monthly transaction volumes exceeding 500,000.[8] In the EU, the digital euro’s planning phase concluded in October 2025, paving the way for technical pilots, concentrating on usability and privacy amid stakeholder engagements.[9] Central banks are encouraging CBDCs to improve efficiency and reduce reliance on the dollar. Emerging economies are concerned with sovereignty, whereas advanced economies are concerned with keeping up with private digital money.

However, the United States stands out as an outlier. In early 2025, President Donald Trump issued an executive order prohibiting federal agencies from pursuing or issuing a US CBDC, citing privacy and sovereignty concerns. This action effectively halted federal CBDC development, leaving the country reliant on private stablecoin initiatives. This hesitancy has given rivals an advantage, accelerating a global digital currency arms race.[10]

Undermining Sanctions Regimes

Sanctions have long been Washington’s major non-military instrument for enforcing global compliance, leveraging the dollar’s dominance in SWIFT (the Society for Worldwide Interbank Financial Telecommunication) and correspondent banking networks to isolate adversaries such as Russia and Iran.[11] CBDCs challenge this paradigm by facilitating direct, peer-to-peer cross-border transactions outside Western-controlled systems. Russia’s development of a digital ruble, for example, facilitates energy payments while circumventing US sanctions imposed during the 2022 invasion of Ukraine, by processing deals in local currencies without the use of dollar intermediaries.[12]

China’s e-CNY epitomises this transition; it is incorporated into the Belt and Road Initiative (BRI) to settle trades with over 140 partner countries, bypassing SWIFT and reducing exposure to US financial pressure. By mid-2025, use of RMB (including the e-CNY) in BRI projects would account for a significant part of non-dollar settlements, allowing sanctioned firms to easily access global markets.[13] Similarly, the mBridge project, a BIS-backed infrastructure incorporating China, the UAE, Hong Kong, and Thailand, tested wholesale CBDC settlements, achieving real-time processing at 0.1-0.3% cheaper costs than SWIFT’s 0.3-0.5%, while safeguarding participants from extraterritorial sanctions.[14]

For India, this advancement has a double edge. As a BRICS member, New Delhi’s digital rupee experiment, which began in 2022 and will be expanded by 2025, positions it to resist prospective US sanctions on critical ties such as oil imports from Russia, many of which have been settled in rupees since 2022.[15] However, over-reliance on Western systems remains a problem; interoperable CBDCs could strengthen India’s autonomy by ensuring that geopolitical tensions do not disrupt commercial flows. Overall, CBDCs are weaponising finance, transforming sanctions from rigid barriers to porous roadblocks in an increasingly fragmented global system.

According to researchers, cross-border CBDC programs are experimenting with new designs in which central banks collaborate directly, minimising dependency on correspondent banks and old systems.[16] This is a significant incentive for countries that detest dollar dominance. And for the United States, the challenge is twofold: maintaining dollar dominance while adjusting to a new digital landscape. A shift away from the dollar will not occur overnight, but the signs are there. According to one study, “introducing a CBDC sooner, rather than later, could give rise to a significant first-mover advantage.“[17]

Transforming Trade Settlements

Global trade, valued at more than $28 trillion per year,[18] has been hampered by a dollar-centric settlement system, resulting in delays and penalties that disproportionately affect impoverished countries. CBDCs promise a revolution by enabling fast, low-cost cross-border payments, thereby promoting de-dollarisation and multipolar trading blocs. The BRICS nations, now expanded to include Egypt, Ethiopia, Iran, the UAE, and Indonesia, have championed this through efforts such as BRICS Bridge and BRICS Clear, intending to establish a payment system based on local CBDCs or a gold-backed “Unit” currency agreed to at the 2024 Kazan summit.[19]

China-Russia commerce, which by 2025 already conducts 90% of settlements in non-dollar currencies, utilises e-CNY and digital ruble for energy transactions, with Shanghai’s International Energy Exchange accounting for 10.5% of global oil futures traded in yuan.[20] The emergence of the petro-yuan, aided by non-dollar oil sales from Saudi Arabia and the United Arab Emirates, demonstrates how CBDCs accelerate this trend, potentially undermining the dollar’s 60% share of global reserves.[21]In Asia, the Regional Comprehensive Economic Partnership (RCEP) combines CBDC platforms, enabling seamless yuan-rupee transactions, lowering remittance costs for India’s diaspora.[22]India stands to benefit greatly from its UPI-linked digital rupee, which could streamline over $100 billion in annual remittances and boost exports to BRICS partners. By 2025, bilateral rupee-ruble transactions had stabilised, with CBDC pilots enhancing efficiency despite Western constraints.[23]

Nonetheless, obstacles remain: interoperability standards are still in their early stages, and the BIS’s Project Agorá, which includes numerous central banks, emphasises the importance of unified norms to avoid fragmentation.[24] As CBDCs continue to spread, global commerce will progressively bypass the dollar, empowering Global South economies and diminishing the West’s gatekeeping role.

The Risks and Fault Lines

CBDCs also pose significant hazards that could exacerbate geopolitical and economic instability. Their centralised ledgers make them excellent targets for state-sponsored hacking or ransomware, with potentially widespread consequences. In BIS simulations, China’s e-CNY revealed vulnerabilities in blockchain interoperability, emphasising the critical need for quantum-resistant security as cyber-espionage grows.[25]

Monetary policy implications exacerbate the situation. Programmable CBDCs enable central banks to impose restrictions such as expiration dates or targeted stimulus, increasing control yet risking inflation manipulation or capital flight in volatile regimes. During crises, if citizens transfer an excessive amount of money from commercial banks to central bank wallets, bank runs may intensify, undermining the credit-creation mechanism. The IMF’s research suggests that poorly structured CBDCs could exacerbate volatility in emerging nations.[26]

The risk of financial exclusion is high if CBDCs replace cash too quickly, alienating the unbanked populations who rely on physical money for privacy and convenience. Despite UPI’s popularity in India, approximately 150 million adults remain outside the formal banking network, emphasising the significance of maintaining a mix of cash and digital options.[27] These fault lines demand balanced regulation to harness the potential of CBDCs without amplifying inequalities or vulnerabilities.

Conclusion

CBDCs are more than just digital currencies; they are instruments of power. They enable states to bypass the dollar-dominated system, reshape global trade, and challenge Western financial hegemony. The real contest ahead is not over cash, but over who controls the digital infrastructure that moves it. Those countries that master these systems will have the ability to redefine the rules of global finance.

In the future decade, the world will no longer ask whether digital currencies matter, but rather, whose system the world will depend on, a question that may ultimately determine the next balance of power in world affairs.

References:

- [1] The Impact of Central Bank Digital Currencies on Regional Power Dynamics

- [2] Central bank digital currencies: foundational principles and core features

- [3] Concept Note on Central Bank Digital Currency

- [4] The geopolitical relevance of central bank digital currencies

- [5] Project mBridge: connecting economies through CBDC

- [6] Recent Global Trends in CBDC Development

- [7] Beyond cash: Will the digital yuan redefine money?

- [8] CBDCs in India: Where Do We Stand?

- [9] Third Progress Report on the Digital Euro Preparation Phase

- [10] Strengthening American Leadership in Digital Financial Technology

- [11] Russia Tried to Isolate Itself, but Financial Ties Called Its Bluff

- [12] Digital Ruble: Concept and Main Directions of Development (Updated 2023–2025)

- [13] High-level technical requirements for a functional central bank digital currency (CBDC) architecture

- [14]Project mBridge reached minimum viable product stage

- [15] Central Bank Digital Currency (CBDC) pilot launched by RBI in retail segment has components based on blockchain technology

- [16] High-level technical requirements for a functional central bank digital currency (CBDC) architecture

- [17] The geopolitical relevance of central bank digital currencies

- [18] Annual change in the merchandise trade volume (imports and exports) worldwide from 2020 to 2023, with a forecast up to 2025

- [19] Outcome of the 16th BRICS Summit in Kazan, Russia

- [20] Russia-China trade almost 100% outside Western currencies – finance minister

- [21] Saudi-China ties and renminbi-based oil trade

- [22] RBI Joins Nexus to Link UPI with ASEAN Fast Payment Systems for Cross-Border Payments

- [23] Rupee-rouble rule: RBI clears path for faster India-Russia payments

- [24] Project Agorá: central banks and banking sector embark on major project to explore tokenisation of cross-border payments

- [25] Central bank digital currency (CBDC) information security and operational risks to central banks

- [26] “Central Bank Digital Currencies and Financial Stability: Balance Sheet Analysis and Policy Choices” (IMF Working Paper, 2024)

- [27] Access to banking

Pranav S is a Project Assistant at the Energy Department, Government of Karnataka with an MA in Public Policy. Views expressed are the author’s own.