- At the heart of this system are three interrelated elements: debt, the dominance of the U.S. dollar, and a pattern of dependency that has evolved over decades.

- The result is a self-perpetuating cycle. Countries borrow to stabilise their economies, implement austerity measures that can suppress growth or exacerbate inequality, and eventually find themselves needing to borrow again.

- For countries in the Global South, this creates a structural vulnerability. When their currencies depreciate against the dollar, the cost of servicing dollar-denominated debt rises automatically.

- Ultimately, the story of debt, the dollar, and dependency is not solely about finance; it is about power, who holds it, how it is exercised, and how it shapes the developmental possibilities available to nations.

There is a system that affects the fate of nations not through war or direct control, but through money. This system operates through loan agreements, currency markets, and rules that most people do not see. Its effects are very clear: reduced funding for public services, recurring debt crises, and limited policy autonomy in many parts of the Global South. We call this system the global financial architecture, and for many developing countries, it feels more like a constraint than a source of support.

At the heart of this system are three interrelated elements: debt, the dominance of the U.S. dollar, and a pattern of dependency that has evolved over decades. Together, these factors shape development trajectories, influence policy choices, and determine the degree of control countries retain over their economic futures.

The Legacy of Debt: A Cycle That Is Hard to Escape

For countries in Africa, Latin America, and parts of Asia, debt is not merely a financial tool; it has become a persistent structural challenge. Borrowing often begins as a necessity: to finance infrastructure, stabilise economies, or respond to crises, but over time, it can evolve into a self-reinforcing trap.

The debt crises of the 1980s illustrate how this dynamic emerged. Many developing countries accumulated substantial external debt during the 1970s, supported by low global interest rates and abundant international liquidity. When interest rates rose sharply in the United States, particularly during the Federal Reserve’s monetary tightening under Paul Volcker, the cost of servicing this debt increased significantly. Countries that had borrowed in U.S. dollars suddenly faced severe repayment pressures, leading to widespread defaults and restructuring.

What followed was a pattern that continues to shape sovereign debt dynamics today. Countries experiencing debt distress often turn to international financial institutions such as the International Monetary Fund (IMF) and the World Bank for assistance. In exchange, they agree to implement policy conditionalities, typically including fiscal consolidation, privatisation of state-owned enterprises, and trade liberalisation. While these measures are presented as necessary for restoring macroeconomic stability, they often entail significant social trade-offs, including reduced public expenditure on healthcare, education, and welfare programs.

The result is a self-perpetuating cycle. Countries borrow to stabilise their economies, implement austerity measures that can suppress growth or exacerbate inequality, and eventually find themselves needing to borrow again. Debt, instead of serving as a tool for development, increasingly functions as a mechanism that prolongs financial vulnerability and limits long-term policy autonomy.

The Dollar’s Dominance: Power That Goes Beyond Borders

If debt is one component of the system, the dominance of the U.S. dollar is another.

Today, a significant share of global trade is conducted in U.S. dollars, and most international loans are denominated in dollars. Central banks also hold a large portion of their foreign exchange reserves in dollar-denominated assets. This confers considerable structural influence on the United States within the global financial system, often described as an “exorbitant privilege.”

For countries in the Global South, this creates a structural vulnerability. When their currencies depreciate against the dollar, the cost of servicing dollar-denominated debt rises automatically. Even when domestic economic conditions remain stable, external shocks such as U.S. monetary tightening or interest rate hikes can generate significant macroeconomic stress.

This dependency on dollar liquidity becomes very clear during crises. When global uncertainty rises, investors tend to shift capital toward perceived safe-haven assets, often located in the United States. This results in capital outflows from developing economies, currency depreciation, and rising borrowing costs. In effect, decisions made in Washington or on Wall Street can transmit financial shocks across borders, shaping economic outcomes in countries thousands of miles away.

Conditionalities and Policy Constraints

When countries require financial assistance during crises, they often turn to institutions such as the International Monetary Fund (IMF). While the IMF provides critical support, it also imposes policy conditionalities designed to ensure repayment and restore macroeconomic stability.

These conditions typically include reducing government deficits, tightening monetary and fiscal policy, and implementing structural reforms. In theory, such measures are intended to restore economic balance; in practice, they can constrain a country’s policy autonomy.

For example, a government facing an economic downturn may seek to increase public spending to stimulate growth. However, under IMF-supported programs, it may instead be required to pursue fiscal consolidation, limiting its ability to deploy countercyclical policies. Similarly, efforts to protect domestic industries may be discouraged in favour of trade liberalisation and market-oriented reforms.

This dynamic creates a tension between financial discipline and domestic development priorities. Governments are often compelled to balance external financial obligations with internal socio-economic demands, highlighting the trade-offs embedded within crisis management frameworks.

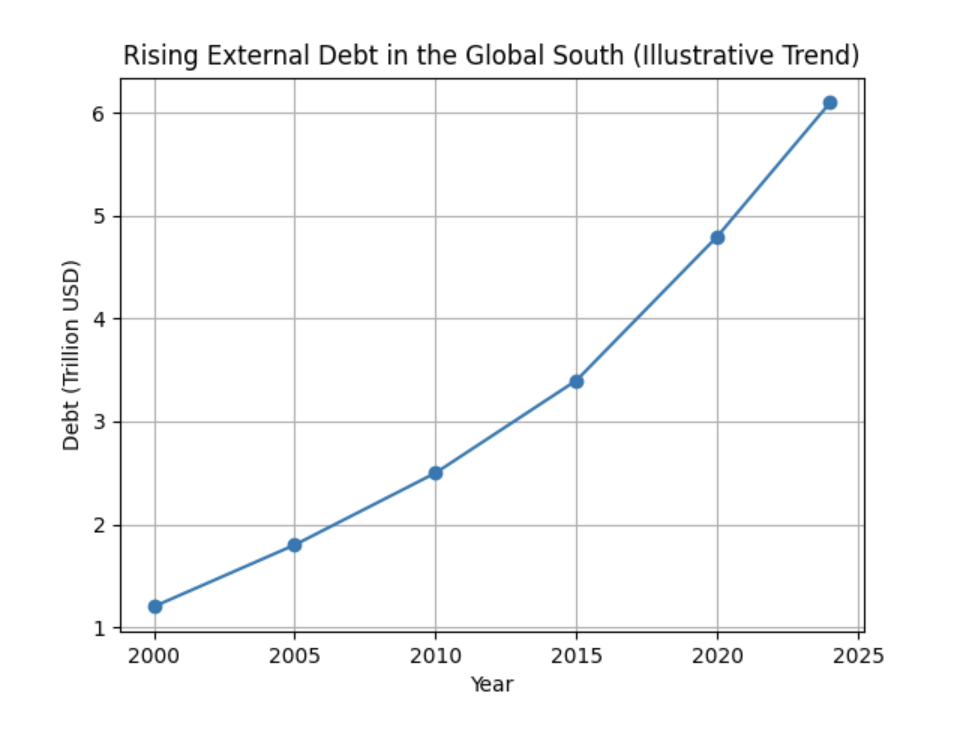

A Visual Snapshot: Debt Stress in the Global South

Across developing countries today, rising debt levels, elevated inflation, and currency depreciation are converging to generate a renewed wave of financial stress. From Sri Lanka’s sovereign default and economic crisis to Zambia’s prolonged debt restructuring process, the pattern is both familiar and concerning.

Dependency Beyond Economics

The effects of this architecture extend beyond economics. They shape policy choices, governance structures, and even international alignments.

Countries that are heavily dependent on external financing may find their foreign policy space constrained. They may prioritise maintaining access to global markets over pursuing fully independent political strategies. Domestic policies can also become influenced by external expectations and financial pressures rather than internally determined priorities.

This is not to suggest a system of overt control or coercion. Rather, it is one in which incentives, constraints, and dependencies interact in complex and often indirect ways. The outcome, however, is often the same: a narrowing of policy space and limited room for manoeuvre.

The Human Dimension

It is easy to discuss debt and currency in abstract macroeconomic terms. However, behind these concepts lie the lived realities of individuals and households.

When governments cut spending to meet fiscal targets, it is often ordinary citizens who bear the cost. Reduced subsidies can increase the price of food and fuel, while cuts in public services can limit access to healthcare and education. Unemployment may also rise as public sector employment contracts are cut.

For many, the effects of global financial structures are not theoretical; they are embedded in everyday life. This human dimension is often underrepresented in policy discourse, yet it is essential to understanding the full socio-economic impact of the system.

India in the Global Financial Architecture: Between Constraint and Leverage

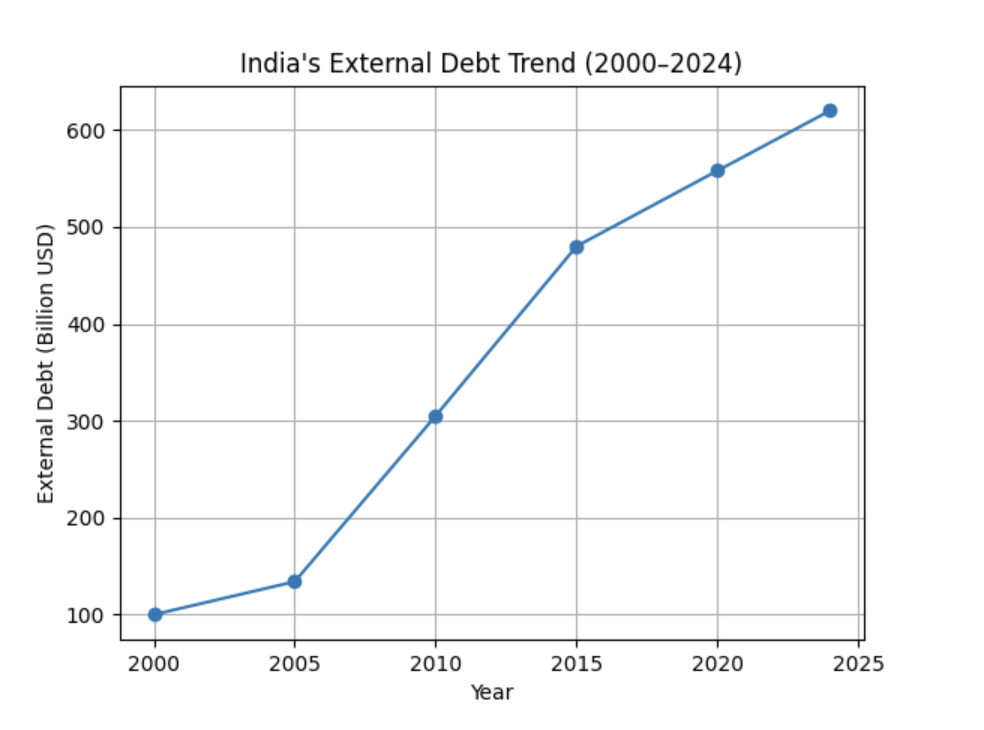

India occupies a distinct position within the global financial system. Unlike many countries in the Global South, it is not in a state of crisis. It has avoided sovereign default, maintains substantial foreign exchange reserves, and possesses a relatively diversified economy. Yet, despite these strengths, India remains exposed to structural pressures arising from debt dependence, dollar dominance, and global financial governance frameworks.

One of the more visible dimensions of this exposure is India’s relationship with external debt. While India’s overall debt levels are generally considered manageable, the composition of that debt introduces specific vulnerabilities. A significant portion is denominated in foreign currencies, primarily the U.S. dollar, which exposes the economy to exchange rate risks. When the rupee depreciates, the cost of servicing this debt rises even if underlying macroeconomic fundamentals remain stable.

This dynamic becomes particularly evident during periods of monetary tightening. For instance, when the U.S. Federal Reserve raises interest rates, capital tends to flow out of emerging markets such as India and back into U.S. assets. This places pressure on the rupee, increases borrowing costs, and forces policymakers to respond often by tightening domestic monetary policy or intervening in foreign exchange markets. In effect, decisions taken outside India’s borders can materially shape its macroeconomic policy choices.

At the time, India’s large foreign exchange reserves served as a critical buffer against external shocks. These reserves provide the Reserve Bank of India (RBI) with the capacity to stabilise the currency and manage exchange rate volatility. However, maintaining large reserves entails significant trade-offs. Resources that could otherwise be invested in domestic development are instead held in relatively low-yield foreign assets, predominantly denominated in U.S. dollars. This reflects a broader reality of the global financial system: macroeconomic stability often requires operating within and aligning with its existing structural constraints.

India’s experience with international financial institutions also reflects a significant evolution over time. During the 1991 balance of payments crisis, India was compelled to seek assistance from the International Monetary Fund (IMF), accepting a series of structural reforms that reshaped its economic trajectory. These reforms, such as liberalisation, privatisation, and globalisation, are widely credited with accelerating economic growth. However, they also marked a moment when external financial pressures played a decisive role in shaping domestic policy direction.

Today, India is no longer just a borrower from the IMF. Instead, it has emerged as a contributor to global financial stability, actively participating in multilateral institutions such as the New Development Bank (NDB) and the Asian Infrastructure Investment Bank (AIIB). This dual role, as both a participant in and a potential shaper of the evolving global financial architecture, sets India apart from many other countries in the Global South.

Yet, the question of policy autonomy remains complex. India must constantly balance competing priorities: maintaining investor confidence, managing inflation, supporting economic growth, and protecting vulnerable populations. Global financial integration brings significant benefits, including access to capital, expanded trade opportunities, and technology and knowledge transfers. At the same time, it also imposes structural constraints on domestic policymaking.

Perhaps the most telling aspect of India’s position is this: it has more room to manoeuvre than many of its peers, yet it continues to operate within the same systemic constraints. It cannot fully escape the influence of the U.S. dollar, nor can it entirely insulate itself from global financial cycles. What it can do and is doing is seek to shape the system from within.

Efforts to promote trade in currencies

Digital currencies and emerging financial technologies also hold significant transformative potential. Central Bank Digital Currencies (CBDCs), in particular, could reduce reliance on traditional banking intermediaries and established financial networks. This, in turn, may facilitate more efficient and cost-effective cross-border transactions.

However, these innovations remain at an early stage of development and adoption. The U.S. dollar continues to be the dominant global reserve and transaction currency, and traditional banking and financial institutions remain central to the functioning of the international financial system. While changes are underway, the transition toward alternative financial architectures is likely to be gradual and uneven.

This system, in which trade, debt, and savings are deeply interconnected through a single dominant currency, illustrates why the U.S. dollar exerts disproportionate influence over global finance.

Can We Reduce Our Dependence On The Dollar?

The question is not whether the system will fundamentally disappear. It is unlikely to do so. The more relevant question is whether countries in the Global South can gradually enhance their control over domestic financial and policy decisions within this system.

Several strategies are already being pursued:

- Strengthening domestic financial institutions to improve debt management and fiscal resilience

- Diversifying export markets to reduce vulnerability to external shocks

- Developing regional financial safety nets and cooperative mechanisms

- Promoting domestic industrial capacity to reduce import dependence

At the same time, there is growing recognition that systemic reforms at the global level are necessary. This includes enhancing the representation of developing countries in international financial institutions, improving access to affordable financing, and establishing more efficient and timely sovereign debt restructuring mechanisms.

Finding A Way Between What We Have To Do And What Is Possible

The global financial system is not static; it evolves in response to economic trends, political pressures, and technological change. However, its core structural features, such as debt dynamics, the dominance of the U.S. dollar, and constraints on policy autonomy, continue to shape outcomes across the Global South.

For countries, the challenge is not simply to exit this system, but to navigate and engage with it more effectively while expanding domestic policy space. This requires strengthening internal economic resilience while also pursuing coordinated reforms at the international level.

There is no single solution. However, there is growing recognition that the current system does not fully support equitable development outcomes. Whether through incremental reforms or more structural transformations, the coming decades will be critical in determining whether the Global South can transition from a position of dependency toward greater economic agency.

Ultimately, the story of debt, the dollar, and dependency is not solely about finance; it is about power, who holds it, how it is exercised, and how it shapes the developmental possibilities available to nations.

Daljeet Singh holds a BTech in Computer Science and is currently pursuing an MA in Political Science. His interests range across geopolitics, international relations, and technology. An avid reader and writer, he is passionate about exploring the intersections of these fields. Views expressed are the author’s own.