- The Salar de Uyuni, which spans an area roughly the size of Jamaica, contains what geologists consider to be the largest lithium reserves in the world.

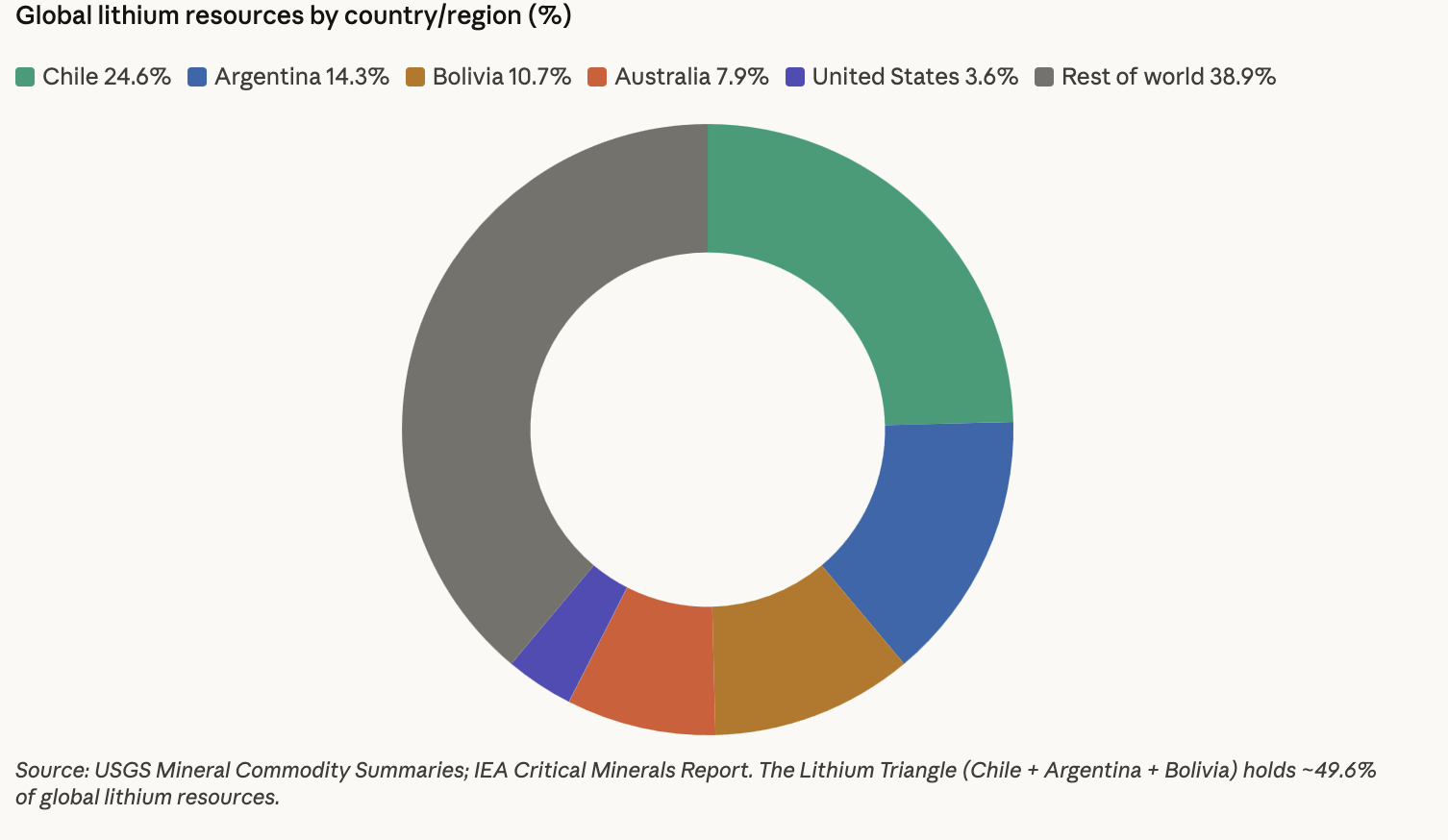

- The lithium triangle alone holds nearly 49.6% of global lithium resources, a figure that translates directly into geopolitical leverage.

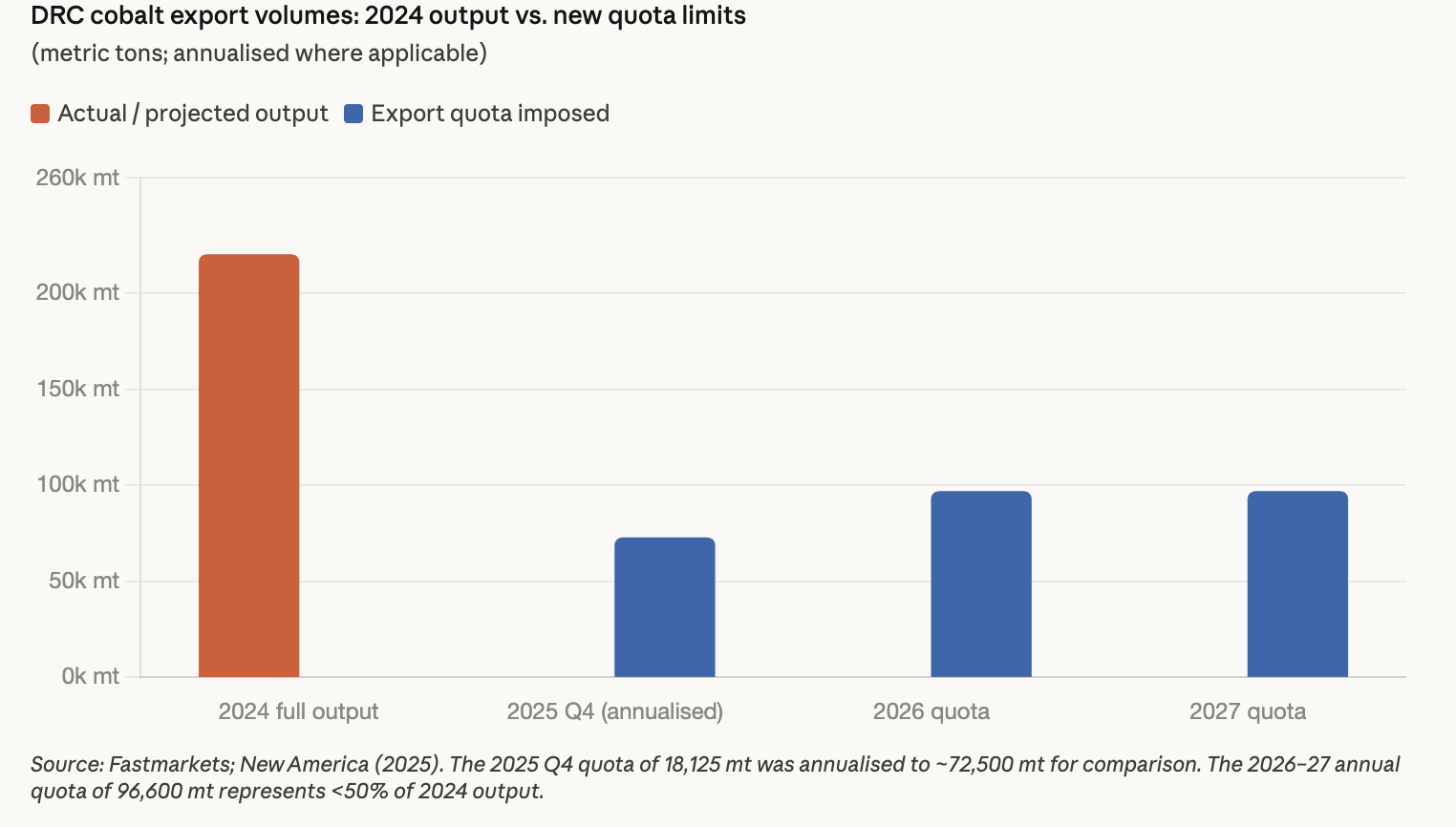

- Under the new quota system, exports have been tightly restricted, with 18,125 metric tons permitted for 2025 and 96,600 metric tons annually for the following two years.

- China’s restriction of the export of rare earths made one reality clear: no country can remain strategically neutral regarding the sourcing of critical minerals.

The southwestern region of Bolivia hosts a vast salt flat at an altitude of 3,600 meters, so expansive and brilliantly white that it is visible even from space. The Salar de Uyuni, which spans an area roughly the size of Jamaica, contains what geologists consider to be the largest lithium reserves in the world, an element indispensable to electric vehicle batteries, grid-scale storage systems, and modern electronics. Yet, the communities surrounding it have endured decades of deep poverty.

This paradox, a nation endowed with resources comparable to oil-rich regions like Saudi Arabia, yet marked by persistent poverty, has defined the relationship between resource-rich developing countries and industrialised economies for generations. What is different today is not the existence of this imbalance, but the emergence of a new global energy order that few anticipated.

The present moment represents a rare historical inflexion point, occurring perhaps once or twice in a century, where a technological transformation is fundamentally reshaping global power structures. The transition from fossil fuels to renewable energy was expected to reduce dependence on traditional petro-states. Instead, it has reconfigured dependency, shifting strategic importance from the Persian Gulf and the North Sea to regions such as the Andes, Central Africa, and Southern Africa.

A New Periodic Table of Power

The “lithium triangle” comprising Chile, Argentina, and Bolivia holds a dominant share of global lithium reserves. Meanwhile, the Democratic Republic of Congo accounts for the majority of the world’s cobalt supply, and nickel reserves are concentrated in countries such as Indonesia, the Philippines, and Brazil. These nations are no longer peripheral actors; they are becoming central to global geopolitics, as they control the critical materials underpinning the green economy.

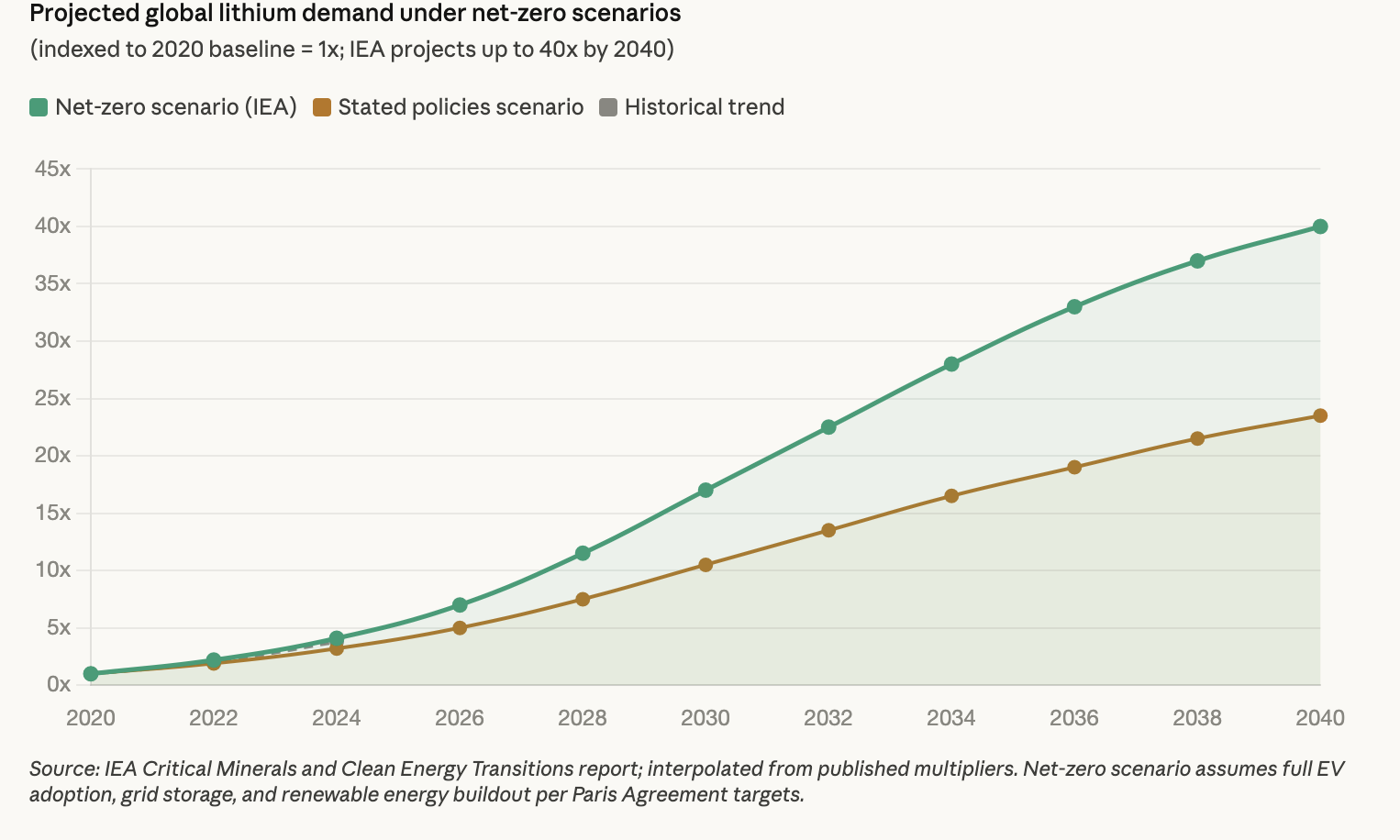

The scale is striking. Chile and Peru together produce approximately 34% of global copper, while Chile, Argentina, and Brazil account for around 32% of lithium output. The lithium triangle alone holds nearly 49.6% of global lithium resources, a figure that translates directly into geopolitical leverage. According to projections by the International Energy Agency, lithium demand could increase fortyfold to meet global net-zero targets.

However, ownership of raw resources has not historically translated into control over value chains. Resource-rich nations have often remained exporters of unprocessed ore, much of which is refined in China, capturing only a fraction of its ultimate value. A ton of lithium carbonate extracted from the Atacama may generate around $6,000 for producers, but once processed into battery cells and integrated into electric vehicles manufactured in cities like Shenzhen, it contributes to products worth over $40,000. The disparity between these figures captures the essence of structural inequity and the motivation behind rising resource nationalism.

The African Gambit

The Democratic Republic of Congo has taken a strategically significant step by introducing export controls on cobalt, a move that would have been politically inconceivable just a few years ago. Under the new quota system, exports have been tightly restricted, with 18,125 metric tons permitted for 2025 and 96,600 metric tons annually for the following two years, representing less than two-fifths of the country’s estimated 2024 production.

The immediate consequences created multiple chain reactions. Cobalt prices experienced sudden fluctuations. The battery manufacturers located in South Korea and Japan rushed to acquire new resources. The DRC demonstrated its ability to drive market changes through its policy decisions, establishing itself as a sovereign nation rather than an area for passive extraction. The entire industry received a warning because it had established a belief system that permitted the transport of African mineral resources to northern and eastern markets on conditions set by purchasers.

The DRC operates as a standalone entity. Zimbabwe established an export prohibition that stops unprocessed lithium ore from leaving its borders. Namibia established a prohibition on lithium exports, which started in June 2023. The President of Malawi declared a complete ban on raw mineral exports in October 2025 because he believed that domestic processing of rare earth minerals would create $500 million in annual revenue for the country.

Collectively, these actions constitute a coordinated and structural shift toward mineral sovereignty across Africa. African nations are increasingly positioning themselves as “global swing states,” leveraging relationships with major powers, including the United States, China, and the European Union, to secure more favourable economic agreements, technology transfers, and industrial partnerships.

Latin America Rewrites the Contract

The trajectory in Latin America is more complex and equally instructive. The Bolivian government signed a $1 billion agreement in late 2024 with a Chinese-led consortium, including CATL, to construct direct lithium extraction facilities in Uyuni, granting the government a 51 per cent ownership stake in each project. This reflects a deliberate effort to maintain majority control over national resources.

Bolivia’s long history of extraction, where wealth from silver, tin, and natural gas failed to benefit ordinary citizens, serves as a cautionary foundation for current policy decisions. Today’s policymakers are acting with a clear awareness of historical inequities.

Chile has adopted a different approach, but with the same objective. President Gabriel Boric introduced a plan in April 2025 requiring all new lithium contracts to operate as public-private partnerships, ensuring substantial state participation. For the first time, indigenous Atacameño communities are being included in governance negotiations, reflecting the reality that these communities have inhabited lithium-rich regions for thousands of years.

Indonesia provides one of the most compelling models. By banning the export of unprocessed nickel and simultaneously developing domestic processing capacity, the country has successfully increased exports of higher-value nickel products. Despite opposition, including a World Trade Organisation complaint from the European Union, Indonesia maintained its policy, prompting Chinese and Korean firms to establish local operations within three years.

South Asia Enters the Game

India’s position is less visible but increasingly significant. Although it does not possess the world’s largest lithium reserves, it holds strategic advantages as a major consumer, processing hub, and diplomatic actor. India’s National Critical Mineral Mission, approved in early 2025, aims to secure supplies of over 30 minerals essential for EVs, renewables, defence, and semiconductors.

In March 2025, Indian officials visited the Democratic Republic of Congo to negotiate cobalt-copper supply agreements, including joint ventures in the Tenke Fungurume mines.

India’s approach differs from both China and the West. It offers technology partnerships rather than debt-driven models, focusing on joint exploration, technology transfer, and long-term supply agreements. This creates mutual alignment—India secures resources, while partner nations gain industrial capacity and diversification away from overdependence on a single power.

When Beijing Pulled the Trigger

A defining moment occurred in October 2025, when the Chinese Ministry of Commerce introduced its most stringent controls on rare earth exports, covering 12 of the 17 rare earth elements, particularly those with the highest strategic value. The timing coinciding with geopolitical tensions, including developments around the APEC summit, was widely interpreted as deliberate. Rare earths ceased to be merely traded commodities; they became strategic instruments of state power.

The consequences were immediate. Supply chains across automotive, defence, and technology sectors faced disruption, with manufacturers warning of potential production halts within weeks. Financial markets reacted sharply, and governments moved quickly to reassess critical vulnerabilities in their supply chains. The episode made one reality clear: no country can remain strategically neutral regarding the sourcing of critical minerals. Supply chains are now integral to national security, and dependencies can be leveraged as geopolitical tools.

The Limits of Leverage

The outcome of this situation remains uncertain because people should not act as if it leads to predetermined results. The resource nationalism research shows multiple warning cases which demonstrate that countries attempting to regain their natural resource control lost everything because they didn’t possess the required technology, stable institutions and viable market options to execute their plan.

Venezuela took control of its oil sector, which resulted in an economic disaster for the country because it possessed the world’s biggest confirmed oil reserves. Bolivia has spent decades pursuing its lithium goals, but until recently, it has only achieved minimal actual lithium production. Bolivia must enhance its infrastructure and legal systems to achieve a level of openness that matches Brazil, Chile, and Argentina because it possesses the most valuable lithium reserves yet remains unable to benefit from them.

The current situation shows different kinds of competitive forces that create challenges for businesses. The project finance methods used by US organisations, the strategic autonomy efforts of EU countries and the 15th Five-Year Plan of China create both limitations and advantages for developing nations.

The United States, together with the European Union, China, India, Japan, South Korea and Gulf states, all compete for your resources, which gives you a stronger negotiating position than you have ever experienced before. The essential task requires us to utilise this opportunity period until sodium-ion batteries, direct air capture and advanced recycling technology emerge as the next technological wave.

The Andean sun continues to create a blinding white appearance on the Bolivian salt flat, which remains untouched. The mining corporations operating from London and Beijing no longer hold exclusive rights to decide who receives advantages from the underground resources. The people who inhabit the surface now possess their first opportunity to participate in decision-making processes that will determine the future of their territory.

References:

- South America’s Lithium Triangle Reshapes Global Trade Through Resource Nationalism — Catalyst McGill (August 2025) https://catalystmcgill.com/south-americas-lithium-triangle-reshapes-global-trade-through-resource-nationalism/

- Lithium Triangle — Wikipedia https://en.wikipedia.org/wiki/Lithium_Triangle

- The Lithium Triangle: Where Chile, Argentina, and Bolivia Meet — Harvard International Review https://hir.harvard.edu/lithium-triangle/

- The Lithium Triangle — Global Business Reports (December 2025) https://www.gbreports.com/contents/the-lithium-triangle/

- Leveraging Latin American Lithium to Mitigate Supply Risks — CGSR / Lawrence Livermore National Laboratory https://cgsr.llnl.gov/sites/cgsr/files/2024-08/Mineral-Security.pdf

- Explainer: Latin America’s Lithium Triangle — AS/COA https://www.as-coa.org/articles/explainer-latin-americas-lithium-triangle

- Latin America’s “Lithium Triangle”: Opportunities and Risks for US Investors — The Oregon Group (October 2023) https://theoregongroup.com/commodities/lithium/latin-americas-lithium-triangle-opportunities-and-risks-for-us-investors/

- Lithium: Here’s Why Latin America Is Key to the Global Energy Transition — World Economic Forum https://www.weforum.org/stories/2023/01/lithium-latin-america-energy-transition/

- Resource Nationalism in the Lithium Triangle — International Relations Review (May 2025) https://www.irreview.org/articles/2025/5/15/resource-nationalism-in-the-lithium-triangle-analyzing-the-investment-environment-for-chinas-projects-in-the-lithium-industry

- Top 4 Largest Lithium Reserves by Country — Investing News Network (March 2025) https://investingnews.com/daily/resource-investing/battery-metals-investing/lithium-investing/lithium-reserves-country/

- The DR Congo’s Cobalt Power Move — New America (November 2025) https://www.newamerica.org/planetary-politics/blog/the-dr-congos-cobalt-power-move/

- Zimbabwe Export Ban a Temporary Dent on Lithium Supply, Says Fitch’s BMI — Mining.com https://www.mining.com/zimbabwe-export-ban-a-temporary-dent-on-lithium-supply-says-fitchs-bmi/

- Zimbabwe’s Lithium Export Ban: China’s Battery Supply Chain in an Era of Resource Nationalism — Modern Diplomacy (March 2026) https://moderndiplomacy.eu/2026/03/25/zimbabwes-lithium-export-ban-chinas-battery-supply-chain-in-an-era-of-resource-nationalism/

- Cobalt Export Quotas: DRC Sets Limits to Rebalance Global Supply — Fastmarkets (September 2025) https://www.fastmarkets.com/insights/drc-cobalt-export-quotas-2025/

- Trade and Domestic Effects of Export Restrictions — OECD (2025) https://www.oecd.org/content/dam/oecd/en/publications/reports/2025/12/trade-and-domestic-effects-of-export-restrictions_fdf21fd0/502e3bcf-en.pdf

- A Coming Clash Over Critical Minerals? — Center for Global Development https://www.cgdev.org/blog/coming-clash-over-critical-minerals

- Zimbabwe Imposes Ban on Exports of All Raw Minerals and Lithium Concentrate — Al Jazeera (February 2026) https://www.aljazeera.com/news/2026/2/25/zimbabwe-imposes-ban-on-exports-of-all-raw-minerals-and-lithium-concentrate

- DRC Lifts Cobalt Export Ban: New Quota System Aims to Stabilize Global Supply and Prices — Investing News Network (September 2025) https://investingnews.com/drc-ends-cobalt-export-ban/

- Inside Africa’s High-Stakes Push for Mineral Sovereignty — Devex (January 2026) https://www.devex.com/news/inside-africa-s-high-stakes-push-for-mineral-sovereignty-111716

- Critical Minerals and India’s Role in a Low Carbon Economy — World Economic Forum (January 2025) https://www.weforum.org/stories/2025/01/critical-minerals-india-securing-low-carbon-global-economy/

- The National Critical Mineral Mission, 2025: Securing Critical Minerals and a Clean Energy Future — IMPRI Impact and Policy Research Institute (July 2025) https://www.impriindia.com/insights/national-critical-mineral-mission-2025/

- Africa’s Mineral Goldmine: India’s Geopolitical Checkmate on China in Critical Minerals Race — Zee News (January 2026) https://zeenews.india.com/india/africas-mineral-goldmine-indias-geopolitical-checkmate-on-china-in-critical-minerals-race-3010093.html

- National Critical Mineral Mission (NCMM): A Strategic Approach to Strengthening India’s Mineral Security — Vivekananda International Foundation https://www.vifindia.org/article/2025/february/13/National-Critical-Mineral-Mission

- China’s Rare Earth Export Controls: Impact and Western Response — SFA Oxford https://www.sfa-oxford.com/market-news-and-insights/sfa-china-s-rare-earth-export-controls-and-their-impact-on-global-supply-chains/

- With New Export Controls on Critical Minerals, Supply Concentration Risks Become Reality — International Energy Agency (IEA) https://www.iea.org/commentaries/with-new-export-controls-on-critical-minerals-supply-concentration-risks-become-reality

- China’s Strategic Rare Earth Export Controls: Geopolitical Impact 2025 — Discovery Alert (December 2025) https://discoveryalert.com.au/china-rare-earth-export-controls-2025-11/

- China’s New Export Controls on Rare Earth and Battery Materials and Technology — Mayer Brown (October 2025) https://www.mayerbrown.com/en/insights/publications/2025/10/prc-announces-new-export-controls-on-rare-earth-and-battery-materials-and-technology

- China’s New Restrictions on Rare Earth Exports Send a Stark Warning to the West — Chatham House (December 2025) https://www.chathamhouse.org/2025/10/chinas-new-restrictions-rare-earth-exports-send-stark-warning-west

- China’s Rare-Earth Export Restrictions — European Parliament Think Tank https://www.europarl.europa.eu/thinktank/en/document/EPRS_ATA(2025)779220

- Ministry of Commerce Notice 2025 No. 61: Announcement of the Decision to Implement Controls on Exports of Rare Earth-Related Items — Center for Security and Emerging Technology (CSET) https://cset.georgetown.edu/publication/mofcom-notice-2025-61/

Daljeet Singh holds a BTech in Computer Science and is currently pursuing an MA in Political Science. His interests range across geopolitics, international relations, and technology. An avid reader and writer, he is passionate about exploring the intersections of these fields. Views expressed are the author’s own.