Two superpowers. One race for the future. How the battle over chips and algorithms is reshaping the global order.

- The contest between the United States and China over artificial intelligence and semiconductor dominance is not merely a business rivalry.

- It is a struggle over who writes the rules of the 21st century: whose infrastructure will power global economies, whose algorithms will shape information, and whose chips will sit inside the weapons, hospitals, and cities of tomorrow.

- If there is a single lever that defines this rivalry, it is the semiconductor.

- When governments treat AI and chips as national security assets rather than commercial products, the rules of engagement change.

- The new cold war, if that is what this is, will not be decided by missiles or proxy armies. It will be decided in fab plants, data centres, university labs, and the everyday choices of billions of users about which AI to trust with their questions.

When historians look back at the 2020s, they may call it the decade when the world split in two — not along an Iron Curtain, but along a silicon one. The contest between the United States and China over artificial intelligence and semiconductor dominance is not merely a business rivalry. It is a struggle over who writes the rules of the 21st century: whose infrastructure will power global economies, whose algorithms will shape information, and whose chips will sit inside the weapons, hospitals, and cities of tomorrow.

The analogy to the Cold War is imperfect but hard to resist. There is the same mixture of fear and ambition, the same race to achieve firsts, the same scramble to win over third nations. The difference is that this time, the battlefield is a fab plant in Taiwan, a GPU cluster in Nevada, or a language model trained on a billion conversations.

The Investment Divide

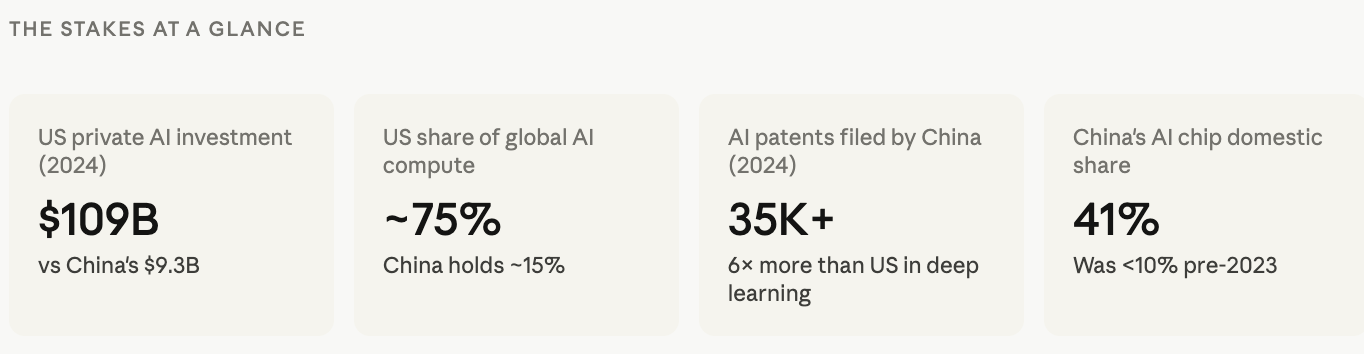

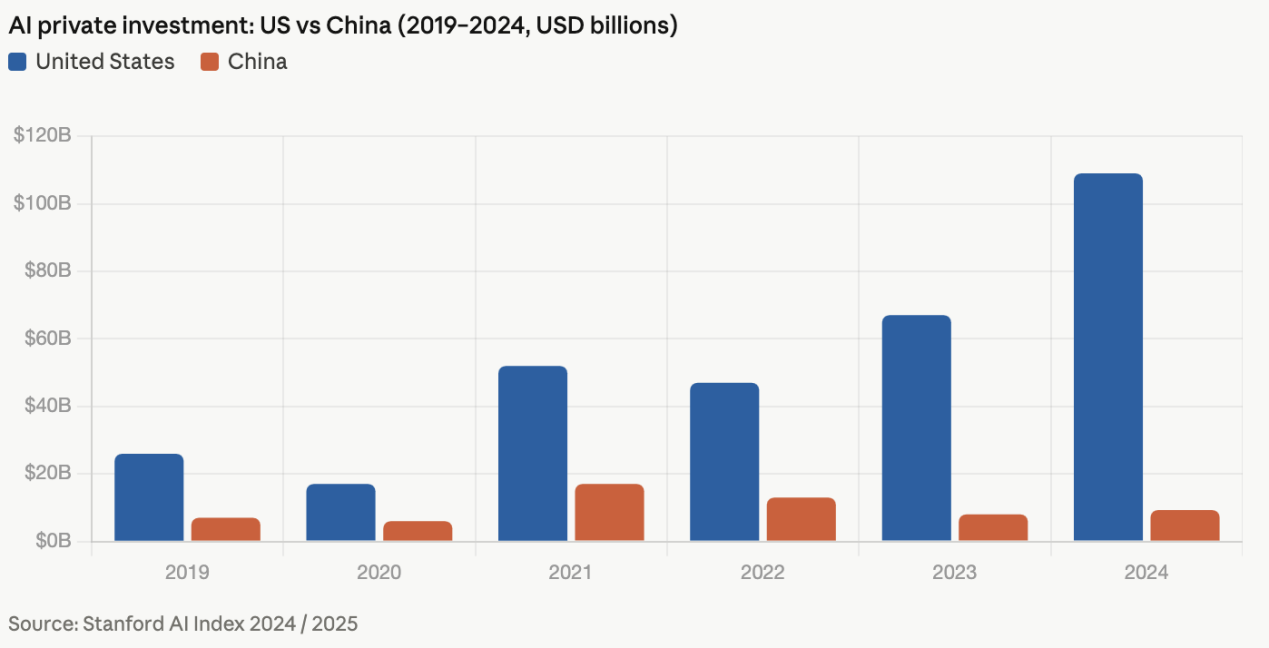

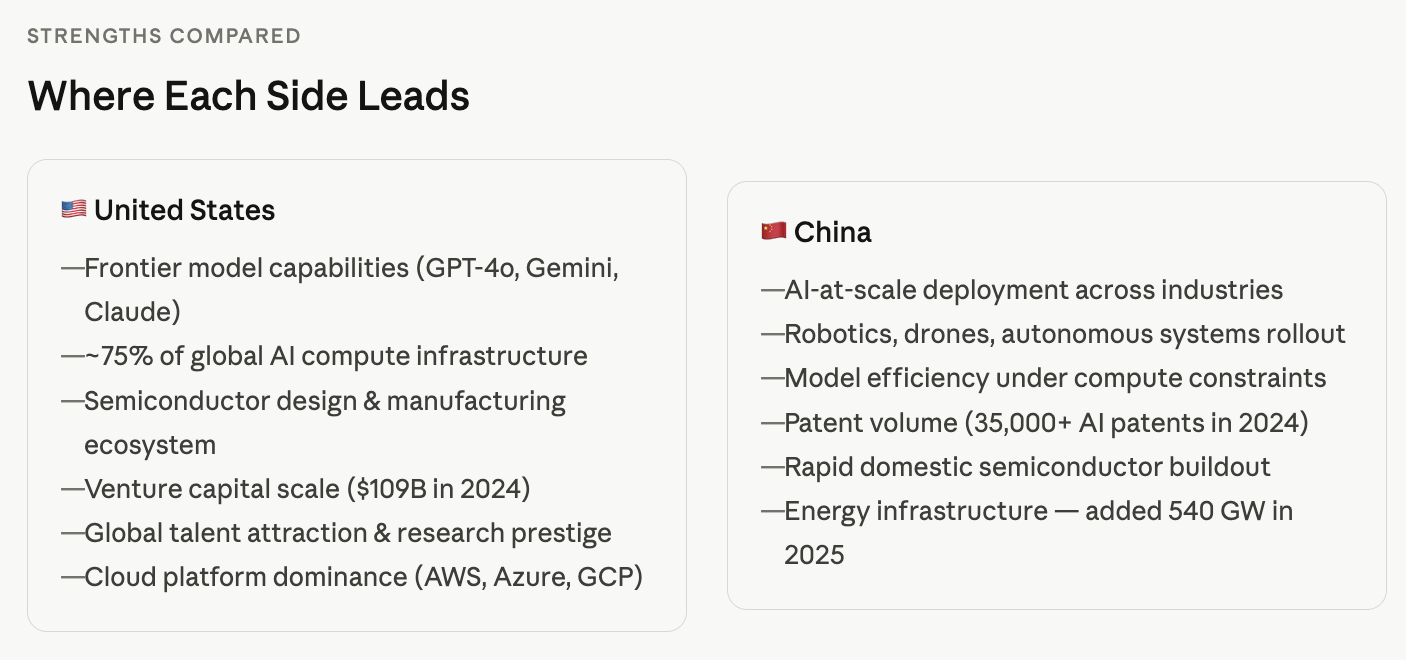

Follow the money and the picture becomes stark almost immediately. In 2024, US companies and investors poured roughly $109.1 billion into AI — nearly twelve times the $9.3 billion deployed in China, according to Stanford’s AI Index. The character of that money differs too. American capital flows primarily from venture funds and tech giants chasing the next breakout product. Chinese capital is more deliberately channelled by the state, through development banks, municipal programmes, and industrial directives like the 2030 AI Development Plan, which commits $150 billion in national funding.

The United States also controls the hardware that makes modern AI possible. Its hyperscale cloud platforms and supercomputing clusters account for roughly 74 per cent of the world’s high-end AI computing capacity. China, despite ambitious targets, currently controls around 14–15 per cent. Microsoft alone spent $80 billion on AI infrastructure in 2025. America’s four biggest cloud companies — Alphabet, Amazon, Meta, and Microsoft — together plan to deploy $650 billion in capital expenditure this year alone.

That kind of spending is difficult to match through state direction alone, and it is creating compounding advantages: better models need more compute, which attracts more talent, which produces better models.

Chips: The Oil Wells of the AI Age

If there is a single lever that defines this rivalry, it is the semiconductor. Advanced chips — measured in nanometres and billions of transistors — are what separate a cutting-edge AI model from a mediocre one. They are also, critically, something China cannot yet make for itself at the frontier.

“Money has never been the problem for us; bans on shipments of advanced chips are the problem.”

— Liang Wenfeng, CEO of DeepSeek, July 2024

Since 2022, the US government has progressively tightened export controls on advanced chips and the equipment used to manufacture them. The logic is straightforward: without access to cutting-edge GPUs, Chinese AI labs cannot train the largest, most capable models. The Semiconductor Industry Association estimated that these restrictions delayed Chinese access to leading-edge training hardware by roughly 12 to 18 months.

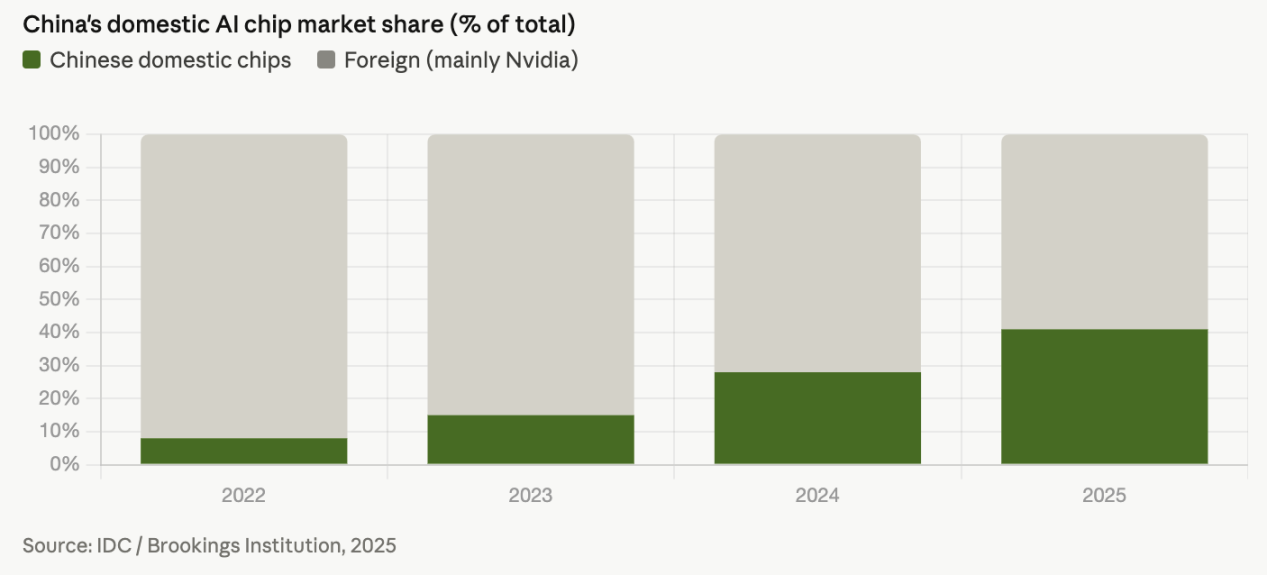

The response inside China has been a furious push toward semiconductor self-reliance. In 2023, Nvidia held more than 90 per cent of China’s AI chip market. By 2025, domestic Chinese chips — led by Huawei’s Ascend series — had claimed around 41 per cent of that market, with Huawei supplying roughly half of those domestic sales. Huawei’s newest Ascend 950PR chips are slated to ship 750,000 units in 2026 alone, while Cambricon plans to deliver 500,000 units of its own AI accelerators, largely manufactured inside China.

The gap at the single-chip level, however, remains large. Chinese AI chips continue to trail Nvidia’s Blackwell and Rubin GPUs on processing performance and memory capacity by a meaningful margin. The contest is real, but the US lead in chip design, manufacturing software, and equipment — shared across the US, Europe, Japan, South Korea, and Taiwan — remains a formidable structural advantage.

Large Language Models and the Sputnik Moment

On January 20, 2025, two events happened simultaneously that seemed to crystallise the rivalry. Donald Trump was inaugurated in Washington. And in Hangzhou, a relatively unknown Chinese startup called DeepSeek released its R1 model — a system that matched the performance of leading American models at a fraction of the compute cost. Analysts called it a “Sputnik moment,” a demonstration that Chinese AI research was capable of genuine innovation, not just imitation.

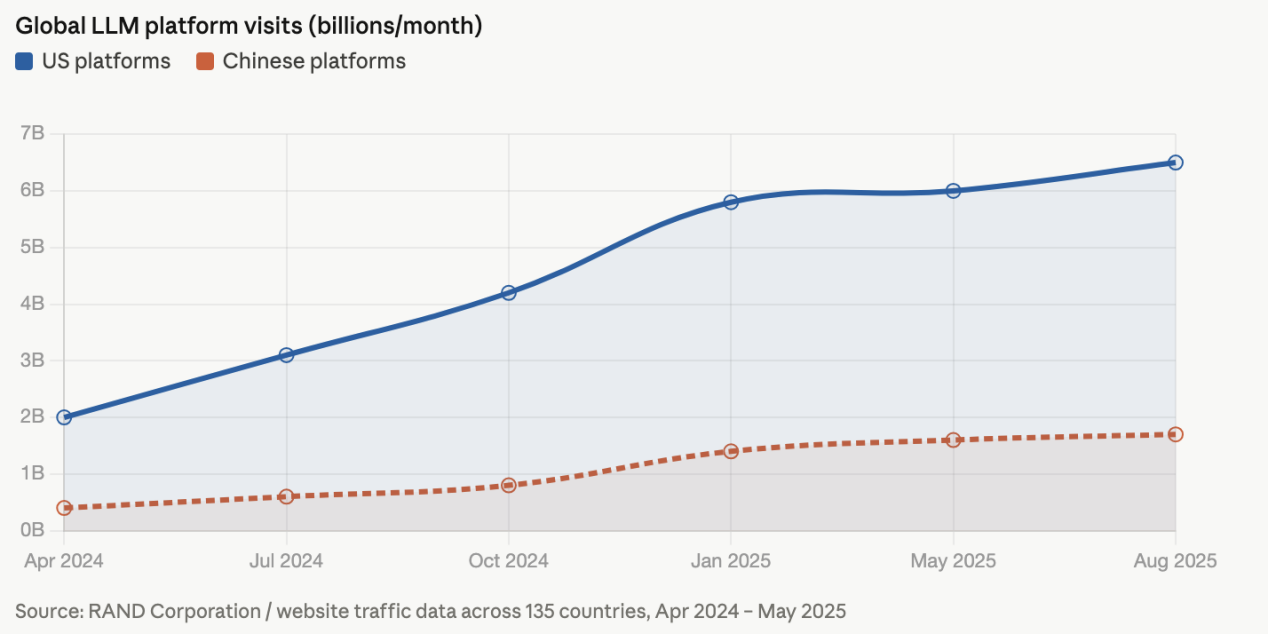

The broader picture, though, tells a story of convergence rather than a sudden Chinese breakthrough. US-based models still dominate in absolute terms. According to Hugging Face data, US-developed models account for 71 per cent of total global downloads. American frontier models maintain a lead across most industry benchmarks — from mathematics and reasoning to code generation and multi-step agentic tasks. China’s top models continue to lag the American frontier by several months or more.

But the direction of travel is unmistakable. Between early 2024 and early 2025, comparisons of Chinese and American models on standard benchmarks showed consistent convergence, particularly where Chinese labs prioritised efficiency — squeezing more performance from fewer chips. China had 302 generative AI service models fully registered and operating as of January 2025, a number that speaks to the breadth and speed of domestic deployment.

The Paper Chase

One of the more surprising corners of this rivalry involves academic research. China published approximately 23,700 AI-related papers in 2024 — a volume that reflects its extraordinary investment in university-industry-government collaboration. In deep learning specifically, China now files six times more patents per year than the United States. The Allen Institute for Artificial Intelligence projected that China would surpass the US in the top one per cent of most-cited AI papers by 2025.

That would represent a significant reversal. For decades, American universities and research labs — from MIT to Stanford to Google DeepMind — have defined the frontier of AI science. China’s “new AI tigers,” companies like Baichuan AI, MiniMax, Moonshot AI, and Zhipu AI, were founded by Tsinghua University faculty and graduates, illustrating how the boundary between academic research and commercial AI has blurred in ways that are accelerating Chinese development.

Chinese companies are also 2.3 times more likely than American ones to deploy AI across multiple business units at scale, according to McKinsey’s Global AI Survey 2024 — a reminder that adoption breadth and raw research capability are different things, and China may be winning one while trailing on the other.

A Surprising Advantage: Powering the Data Centres

One dimension of this rivalry rarely appears in headlines: electricity. Training large AI models is extraordinarily energy-intensive, and both countries are facing the consequences. The International Energy Agency estimates that US data centre power demand will more than double by 2030, reaching 426 terawatt-hours — roughly 9 per cent of total US electricity demand. Permitting delays, grid interconnection bottlenecks, and transformer shortages are slowing American data centre expansion in ways that are genuinely concerning to US policymakers.

China, by contrast, has a remarkable ability to build and connect new power generation. In 2025, China added over 540 gigawatts of new electricity capacity, about 80 per cent from solar and wind. Over four years, China built the equivalent of the entire US power grid in new generating capacity. For AI infrastructure, that is a structural advantage that money alone cannot quickly replicate in a democratic system with extensive permitting requirements.

This Is Not Just About Technology

CIA Director Bill Burns described technology as the “main arena” of the US-China rivalry. That framing matters. When governments treat AI and chips as national security assets rather than commercial products, the rules of engagement change. Export controls, industrial subsidies, talent restrictions, and supply chain decoupling all become legitimate tools of statecraft.

China’s Made in China 2025 initiative explicitly targets semiconductor self-sufficiency. America’s CHIPS Act pours federal money into domestic chip fabrication. Both countries are using state power to reshape markets that once operated on comparative advantage and open trade. The rest of the world — from India to the European Union to Southeast Asia — is being asked, implicitly or explicitly, to pick a side in terms of which chips run their systems, which cloud platforms store their data, and which AI models advise their citizens.

Goldman Sachs’ analysis concludes that the US has maintained its advantage in frontier research and platform-level capabilities. Brookings Institution analysts note, however, that China is “moving ahead in large-scale practical deployment” — rolling out robotics, autonomous vehicles, and AI-embedded infrastructure at a speed that reflects both state coordination and sheer market scale.

How This Ends — Or Doesn’t

It is tempting to call a winner, but the reality is that this race has no clear finish line and no single scoreboard. The US leads in the hardware layer and in the frontier model layer. China is closing gaps in the application layer and building the industrial and energy foundation for long-term competition. DeepSeek demonstrated that compute constraints can, at least in some cases, be partially overcome with algorithmic cleverness.

What is certain is that the next five years will be decisive. US export control policies remain in flux — the Trump administration approved exports of Nvidia’s H200 chips to China in late 2025, a decision critics called a strategic misstep that could provide Chinese labs with more than 890,000 advanced GPUs. China’s domestic chip capabilities, while still behind, are no longer negligible. And the global AI market is being contested in real time across 135 countries, with Chinese platforms steadily gaining ground outside the Western world.

The new cold war, if that is what this is, will not be decided by missiles or proxy armies. It will be decided in fab plants, data centres, university labs, and the everyday choices of billions of users about which AI to trust with their questions. The silicon curtain is already rising — and its consequences will be felt for generations.

References:

[1]Stanford AI Index 2024/2025 — Investment, research output, compute comparisons aiindex.stanford.edu

[2]Brookings Institution — Competing AI strategies for the US and China (April 2026)brookings.edu/articles/competing-ai-strategies-for-the-us-and-china

[3]RAND Corporation — US-China Competition for AI Markets (Jan 2026)rand.org/pubs/research_reports/RRA4355-1.html

[4]RAND Corporation — Full Stack: China’s Evolving Industrial Policy for AI (July 2025)rand.org/pubs/perspectives/PEA4012-1.html

[5]TIME Magazine — 6 Graphs That Show Who’s Really Winning the US–China AI Race (Jan 2026)time.com/7358519/ai-china-us-race-graphs

[6]Recorded Future / Insikt Group — Measuring the US-China AI Gap (May 2025)recordedfuture.com/research/measuring-the-us-china-ai-gap

[7]McKinsey Global AI Survey 2024 — Enterprise adoption ratesmckinsey.com/capabilities/quantumblack/our-insights/the-state-of-ai

[8]Semiconductor Industry Association — 2025: State of the US Semiconductor Industrysemiconductors.org/state-of-the-us-semiconductor-industry

[9]MUFG Americas — Nvidia vs. Huawei AI Chip Capabilities (Dec 2025)mufgamericas.com — AI Chart Weekly: Chip Wars

[10]Tandfonline — China’s semiconductor conundrum: US export controls and their efficacy (2025)tandfonline.com/doi/full/10.1080/23311886.2025.2528450

[11]Outlook Business — US vs China Tech Race 2025: Who Leads in AI, Semiconductors & Robotics outlookbusiness.com — US vs China Tech Race 2025

[12]Second Talent — USA vs China in AI & LLM: Statistics & Market Analysis 2025secondtalent.com/resources/usa-vs-china-ai-llm-statistics

Divyanka Tandon holds an M.Tech in Data Analytics from BITS Pilani. With a strong foundation in technology and data interpretation, her work focuses on geopolitical risk analysis and writing articles that make sense of global and national data, trends, and their underlying causes. Views expressed are the author’s own.